Earlier this month, an article on CoinDesk caught our attention. The flashy headline had something to do with it — “The American Empire Is in Decline. Time for a New Economic System” — but also the ideas and arguments throughout held up their end of the bargain.

So, we reached out to the writer, Lex Sokolin, who is Global Fintech Co-Head at the blockchain software company ConsenSys. Before joining ConsenSys, Sokolin had spent years building companies, designing robo-advisors, and looking at both AI and blockchain. His piece on Coindesk argued that the American financial system was broken and needed a radical fix to stay at the center of the world. We wanted to hear more about how he saw the future of American finance.

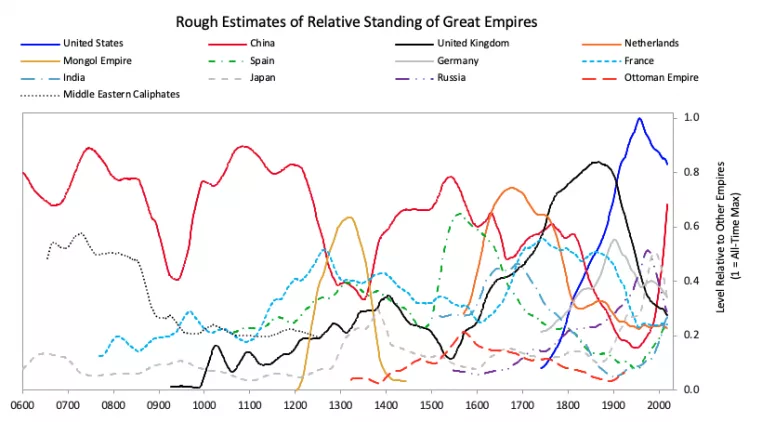

Unifimoney: I reached out after reading your article on Coindesk, “The American Empire Is in Decline. Time for a New Economic System.” In it, you argue that we’re entering a depression-like moment for the American dollar, which could lead to the end of the American Empire. What led you to that conclusion?

Lex Sokolin: So I have to give real credit, or, I guess, cite the bibliography: I was referencing a lot of the thinking that Ray Dalio, who runs a large hedge fund called Bridgewater, did in trying to analyze macroeconomic cycles. And macroeconomic cycles, not just in the terms of this decade and next decade; more like, what does 80 years of an economy look like? What does a century look like? What does 500 years look like? And in that thinking, he tied the concept of a currency to the idea of the strength of an empire and what makes a nation strong and what are the attributes that make it competitive on a global basis.

The work that was really interesting for me was the sequence of attributes that a country goes through. You start with things like investment in education and cheap labor and building out global influence and building out trade. That is followed by the creation of a financial sector that allows for credit and for borrowing and then for trading and the enablement of commerce. That is then followed by the ability to afford the military and hard power and global influence. Then, finally, that allows for the privilege of having a reserve currency. With the reserve currency, you essentially get a get-out-of-jail card for being able to mint money and having everyone else denominate their economic activity in your money, which allows you to control the flow of credit in a very powerful way.

You can retain that advantage of the reserve currency for decades while the sort of foundational attributes of your strength erode. In particular, you can see it in the overextension of credit. People want to preserve the growth and the increase in the standard of living and the quality of living that we’ve had historically — not keep it flat, but at a growth rate relative to the past. In order to do that, more credit is generated in order to create spending and so on. And so, these macrocycles, these 100-year cycles, involve essentially too much borrowing which you’re doing because you have the reserve currency. Countries end up in this position where they have too much debt and start having defaults and runs on various parts of the financial system. Those kinds of moments shine a light on the need for a harder currency that’s not just backed by the faith in the government, but backed by gold or backed by a digital asset or some other obligation. That’s the argument I was trying to pull out, especially as it relates to the responses of the central banks in the west to COVID and the quarantine and the monetary expansion and the fiscal expansion that they’ve had to do in response to the gigantic economic shock.

Unifimoney: In the piece, you talk about the rise of gold and bitcoin currencies at a moment like the one you’re projecting. What will that look like for the people who invest in bitcoin and gold?

Sokolin: There’s a straightforward argument which is based on the idea that governments are going to try to supplement the economic shock and the loss of spending power that households have with various forms of stimulus — whether it’s sending people $1000 in their mail or whether it is buying up a whole bunch of corporate bonds so the asset values in the financial markets don’t collapse and therefore 401Ks can retain value and still get paid out. So, the conventional argument would be that as output stays the same but you have more money circulating around, money would be worth less. And then you’d start having inflation. If that’s the case, then assets that are inflation hedges — such as a variety of commodities like gold and bitcoin — would rise in value relative to the currency that’s being inflated away.

I think it’s a very powerful narrative, but I don’t know which side of the argument I’m on right now. It’s a really complex system, the economy; it’s not this straightforward. So, for example, putting money in the hands of people doesn’t necessarily mean they’re going to spend it, or if they do, they might spend it on essentials and the velocity of money might slow down. So, overall, your spending doesn’t create inflation. It can also be true that if you don’t do the distribution, then the economy will actually shrink a lot more. So, it’s a really complex question.

Unifimoney: We’ve decided to offer the ability to invest in gold and precious metals through our account. You used the term “inflation hedges” — in your view, how important is it for high-earning millennials to diversify their holdings with gold and alternative currencies?

Sokolin: I come from an asset allocation place: portfolio management and risk management are the backgrounds that I bring. I spent a bunch of time in large wealth and asset management companies and, from building a robo-advisor, I’m very used to looking and thinking about pie charts. So, I think the prudent answer — which is not financial advice — is that you need to have an asset allocation that’s exposed to as many types of things as possible, and the more types of different things that are driven by different types of events in the real world, the better it is for you. Gold and bitcoin and commodities and real estate should absolutely, no question, be a part of everyone’s portfolio. Whether you’re a millennial or an older, more risk-averse investor, there is absolutely the need to have exposure to that. Whether it is 2% or whether it is 20% is kind of the flex.

I wouldn’t recommend people go out and lever up 40x on BitMax to get exposure to bitcoin because they know The Happening is happening and so now is the time. I would say, eat a balanced meal and not too much of it, and that gold and bitcoin can drive really good risk-adjusted returns in moments where traditional asset classes are failing.

Unifimoney: You end your piece with “Now is not an incremental time….Now is a time for building the future of the world.” What has the financial system gotten wrong or not done to meet this time you view as a crisis moment?

Sokolin: It’s funny you’d bring that up right after my point about how you should eat a balanced meal. I think that really comes from a place of frustration with FinTech in the last ten years. We have RobinHood and Revolut and Stash and Acorns and Betterment and Wealthfront and SoFi and Lending Club and Venmo and Square and every single thing in the world and, fundamentally, nothing has really changes about financial services. It’s kind of like, we are talking about having a Spotify of CDs, like a really slick frontend for the same old stuff. And so, I was ending that with a wakeup call to say, let’s engage with blockchain and bitcoin and Ethereum on their own terms and think about, ‘What if this wasn’t the edge case? What if this was the only case?’ Now is the time to do this, because the crisis is putting people into a place where they’re willing to try stuff and adopt new solutions.

The above does NOT constitute an offer, solicitation of an offer, nor advice to buy or sell specific securities. The opinions listed above are not the opinions of Unifimoney Inc. or Unifimoney RIA, Inc. but represent the opinions of independent contributors. These contributors may or may not hold positions in the stocks discussed. Investors should always independently research any stocks listed and form their own opinions, while recognizing that any investments made may lose value, are not bank guaranteed and are not FDIC insured.